Preview of the FOMC Meeting: Hints on Interest Rate Path in 4Q Could be the Key Thing to Watch

Greenback index continues to consolidate in a tight range on Wednesday in the run-up to the FOMC meeting. The range has been forming for about a week and indicates short-term equilibrium in USD supply and demand before the release of key market information. The presence of the pattern suggests that a breakout on Fed information will indicate the direction of a fresh trend leg. From a technical perspective, the market looks poised to test the lower edge of the channel (105.70-106) before possible resumption of the upside:

The risk of surprise in the policy today is quite low, according to Fed funds rate futures, the chance of a 75 bp rate hike is more than 90%. At least two Fed speakers stated unequivocally that they will vote for 75bp, leaning towards the idea that the US inflation spike in June above 9% was transitory. In addition, data from the U. Michigan showed that inflation expectations declined in July, which in fact is one of the key goals of the Fed’s monetary tightening. It’s also important to note that the Fed rarely goes against market consensus, so most likely today we will see a rate hike of 75 bp and a lack of significant market reaction to this outcome.

Instead, market participants can focus on hints that may help to assess the size of rate hikes in 4Q meetings. Current consensus on market estimate of the rate path suggests that the Fed will deliver 50 bp in September and 25 bp in November and December. Any surprises in this direction will likely determine short-term demand for USD and US Treasuries of shorter maturity.

The Fed will not release updated economic forecasts or a Dot Plot at today's meeting, so keep in mind that Powell's press conference and FOMC statement will be the main sources of information.

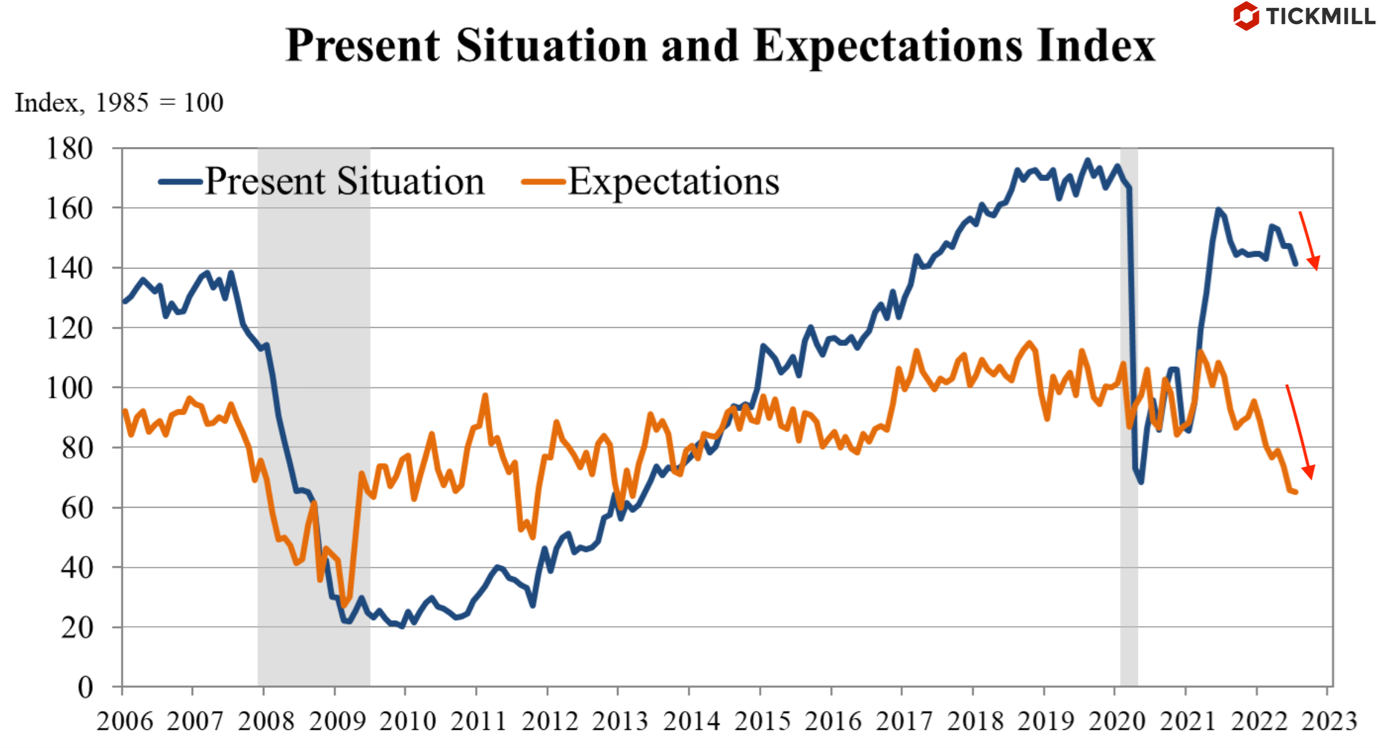

The Conference Board's report on consumer confidence, released yesterday, pointed to a weakening US expansion in the third quarter. The key indicator has been declining for the third month in a row, although not as fast as in June. The current conditions index, based on consumer assessments of business prospects and the state of the labor market, fell from 147.2 to 141.3 points. The Expectations Index also moved lower, but the decline turned out to be insignificant - from 65.8 to 65.3 points:

Inflation expectations, according to the CB report, fell to 7.6% from 7.9% in June.

The moderately weak report and the signal of easing inflation expectations have become another argument in favor of the fact that the Fed will be cautious today, raising the rate by 75 bp and will likely hint at a slowdown in the pace of policy tightening in line with current expectations.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.