Softer Outlook For NZD Economy

The release of the NZIER’s Quarterly Survey of Business Opinion suggests an increased likelihood that we could see negative rates in New Zealand at some point in the future. Currently, the RBNZ projects that the level of rate cuts and fiscal easing in play will be enough to fuel a pickup in economic growth, taking GDP back to the 3% and inflation back to 2%. However, recent data sets do not support this view. Indeed, the ANZ Survey and the NZIR QSBO both suggest that growth is more likely to head down to 1% before it heads up to 3%.

One of the key reasons why activity is likely to remain weak is that investment looks like it will remain constrained. This is not due to interest rates being high (given the recent cuts) but due to downward pressure and growing economic uncertainty. This dynamic was highlighted in the QSBO with machinery investment intentions at a paltry -3%, their lowest level since 2009. Even the “intention to invest in buildings” number, which is usually fairly resilient, turned lower.

Lower Profitability Among Businesses

The data also made a negative impact on profitability, as a result of rising costs, clear. 33% of businesses survey reported that costs were rising while 1% said that selling cost had declined. As a result, this means that 32% of businesses highlighted reduced profitability, which is at its weakest level since 2010.

The weakness in selling prices is a bad omen for inflation expectations and in turn, inflation. This is the dynamic we saw in the ANZ survey this week and while it was possible that the survey was giving a distortedly negative picture due to its weighting to the agricultural sector, the fact that the QSBO backs this picture up is confirmation given that the QSBO misses the agricultural sector completely.

One of the biggest issues facing businesses in the survey was weakening demand. Alongside capacity constraints, 55% of businesses reported that weak demand was the biggest issue preventing them from increasing their output. Although this is lower than the 80% readings typically seen during a recession, it is still well above the 42% reading recorded three quarters ago and is at its highest level since 2015.

Added to this, the QSBO also showed clear signs of labour retrenchment as businesses aim to cut costs. 10% of businesses reported lowering staff numbers, marking the second consecutive quarter of decline for labour levels.

Despite the negative picture painted by the QSBO, we didn’t see much reaction in the NZD. Currently, the market is pricing in two further rate cuts in line with the guidance given at the RBNZ’s last meeting. However, risks seem skewed to the downside and the chance of a further, larger-than-expected rate cut offer opportunities.

Bullish Risks

The risk to this picture is that we see progress with US/China trade talks. If both sides can agree an interim deal at the upcoming talks on October 10th, this could take a lot of pressure off the RBNZ in the short term and allow it to pause its easing program. In this instance, given the expectations for further rate cuts, the move higher in NZD could be sharp.

Technical & Trade Views

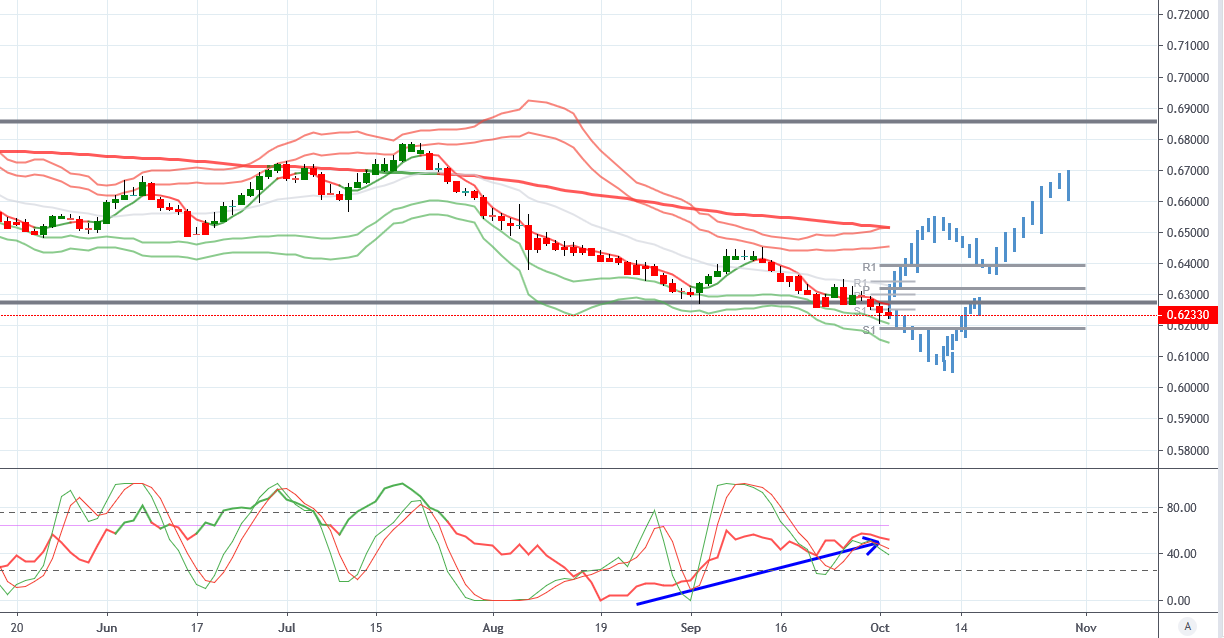

NZDUSD (Neutral, Bearish below .6395, bullish above)

NZDUSD from a technical and trade perspective. NZDUSD has traded down to record new 2019 lows. With long term VWAP still bearish, another leg lower cannot be ruled out. If we push lower from here I will be monitoring a retest of the yearly S1 to position for further downside. However, bullish divergence in momentum studies flag the risk of an upside reversal. If we break back above the monthly pivot, price could be setting up to make a move back up towards long term VWAP.

Please note that this material is provided for informational purposes only and should not be considered as investment advice. The views discussed in the above video are those of our analysts and are not shared by Tickmill. Trading in the financial markets is very risky.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!