Institutional Insights: UBS FX: GBP - Where Is the Risk?

GBP: Where Is the Risk?

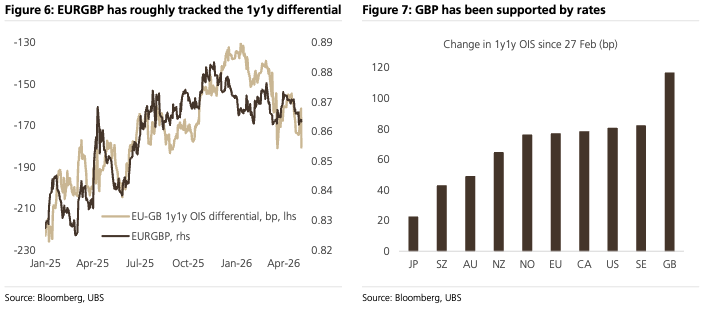

GBP has been surprisingly resilient since the start of the Middle East conflict, helped by a sharper repricing higher in UK front-end rates than elsewhere, broadly constructive risk sentiment, and low implied volatility supporting carry. EUR/GBP has broadly tracked the EU-UK 1y1y OIS differential, and GBP has screened as one of the bigger beneficiaries of the global rates repricing. That said, the strength is not entirely intuitive given the UK faces a negative growth/inflation shock from higher energy prices, long-end gilt yields are at their highest levels since 1998, and local elections tomorrow could become a catalyst for renewed leadership pressure on PM Starmer from the left of the Labour Party.

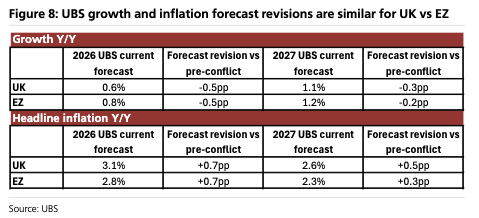

The first reason GBP has held up is that investors may be treating the UK and euro area energy shock as broadly symmetric. UBS economists see the UK as marginally more exposed than the euro area in aggregate, but the actual forecast revisions look very similar. UK 2026 growth has been cut 0.5pp to 0.6%, while eurozone growth has also been cut 0.5pp to 0.8%. Headline inflation has been revised +0.7pp in both regions for 2026, to 3.1% in the UK and 2.8% in the eurozone. In other words, there is not yet enough relative macro divergence to force a meaningful EUR/GBP repricing. The UK looks vulnerable, but not uniquely vulnerable versus Europe.

The second reason is that higher gilt yields have not yet become a fiscal stress story. The long end has moved materially, but the move has been directionally consistent with global duration, and the 30y gilt/Treasury spread is not yet back to pre-November budget stress levels. For GBP, long-end yields tend to matter most when they threaten to wipe out fiscal headroom and force a fiscal event — either looser rules or higher taxes. That is not yet the case. The Chancellor had £23.6bn of headroom at the March OBR update, and although rates have moved sharply since the OBR’s conditioning window — 1y SONIA +78bps, 10y gilts +53bps, 30y gilts +51bps — the fiscal arithmetic has not yet deteriorated enough to create an obvious GBP shock.

The OBR sensitivities are important here. A 1pp sustained rise in gilt yields and policy rate expectations adds around £15bn to public sector net borrowing in 2030-31. A 0.1pp decline in nominal GDP growth each year adds £8bn, while a 1pp rise in RPI inflation adds £11bn. These are persistent multi-year shocks, not one-off moves. So for now, the market can rationalize the gilt selloff as uncomfortable but not yet destabilizing. That may explain why GBP has not responded more negatively to the rise in long-end yields.

The more immediate risk is political. EUR/GBP implied volatility remains very suppressed despite prediction-market odds implying a meaningful probability of Starmer leaving office by end-Q2 and an even higher probability by year-end. That looks complacent on the surface. The local elections could matter if a poor Labour result triggers a leadership challenge from the left, particularly if the campaign rhetoric points toward looser fiscal rules, market-unfriendly tax increases, or materially higher public spending. In that scenario, the combination of higher gilt yields, reduced fiscal headroom and political instability could quickly become a GBP-negative mix.

That said, the setup is not one-way. The market is already broadly bearish GBP anecdotally, and a poor Labour result has been well flagged for some time. If the election outcome is bad but not disorderly, and if there is no credible path to a major fiscal policy shift, GBP could actually strengthen further as event risk is cleared. Systematic selling of EUR/GBP vol has also helped suppress ranges, meaning spot could move aggressively if it breaks either side of the recent 0.85–0.88 range, but an uneventful outcome could leave vol crushed and carry trades intact.

Trading takeaway: GBP’s resilience is explainable, but the risk/reward still looks asymmetric into the election. Rates support and carry remain GBP-positive, while the UK’s fiscal position is not yet under enough pressure to force a gilt-led sterling selloff. But the market is underpricing political/fiscal tail risk, especially given suppressed EUR/GBP vol and the potential for a leadership challenge to revive concerns around fiscal credibility. The base case may be contained price action, but the cleaner risk is still for higher EUR/GBP and higher GBP vol if local elections trigger a more hostile political narrative.

Preferred stance: stay tactically cautious on GBP into the event. Maintain a near-term upside bias in EUR/GBP, with 0.89 end-Q2 still plausible if politics and gilts begin to interact negatively. However, avoid over-sizing the trade given bearish GBP sentiment is already widespread and any “less bad” political outcome could squeeze sterling higher.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!