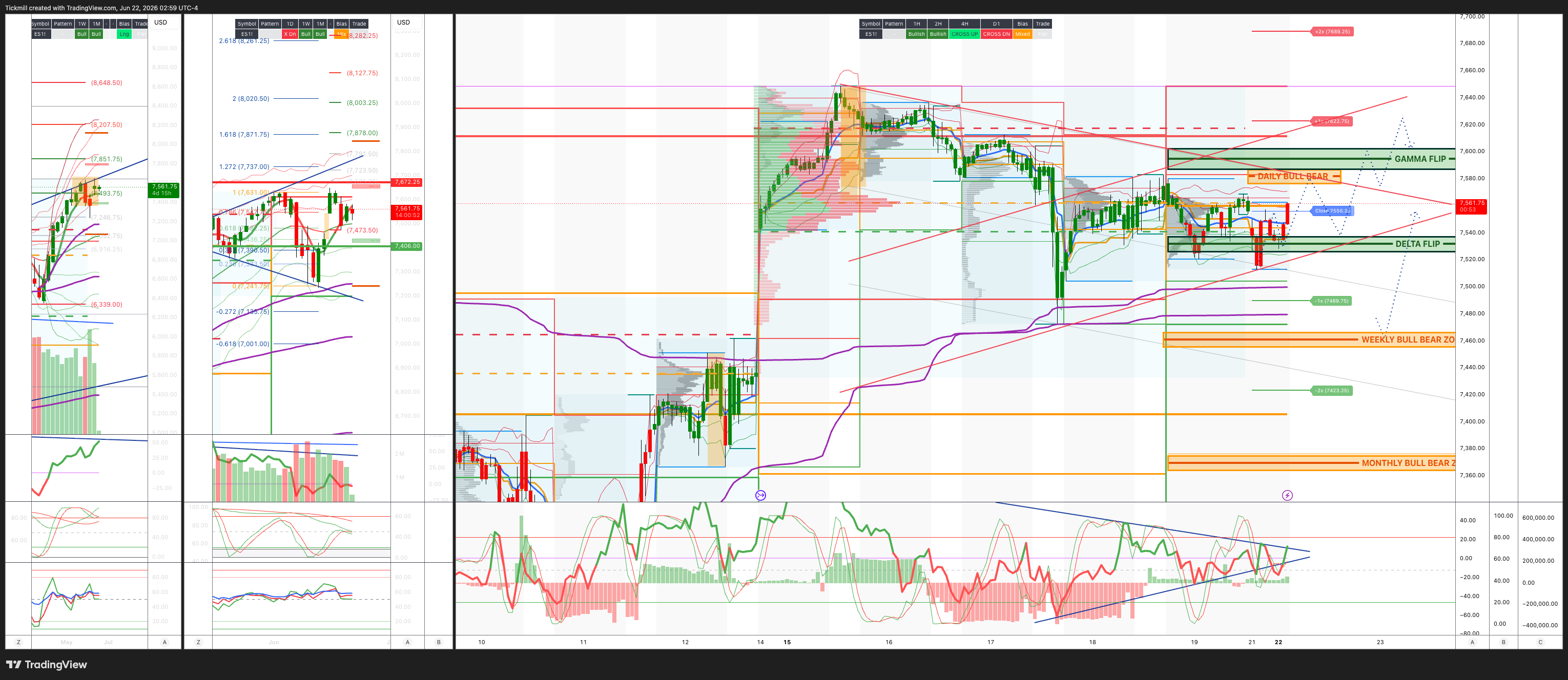

S&P500 Daily Action Areas & Price Targets 22/6/26

S&P500 Daily Action Areas & Price Targets 22/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7560/50

WEEKLY RANGE RES 7692 SUP 7448

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 0.94 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7573

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFL - 7581

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 757585

GAMMA FLIP 7595

DELTA FLIP 7530

DAILY RANGE RES 7622 SUP 7489

2 SIGMA RES 7689 SUP 7423

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH CLOSE

LONG ON ACCEPTANCE ABOVE GAMMA FLIP TARGET 7622 >ATH

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘More Lenght: More Voaltiltity’

The core client debate has clearly shifted. Investors are not asking whether AI is over; they are asking how to own it from here. That is an important distinction because the secular backdrop remains intact, and arguably continues to strengthen across both the US and Asia. Capex expectations are still robust, earnings revisions are still moving higher, and US technology continues to see significant inflows. The fundamental AI story is not breaking. What is changing is the market structure around it.

Prime Brokerage data reinforces that point. Semis are on pace to finish as the most net bought global subsector for a second consecutive year, and net allocations are now at record highs. That is both a bullish confirmation and a risk flag. It confirms that investors still see Semis as the cleanest expression of the AI buildout, particularly through compute, memory, HBM, networking, and data-center demand. But record allocation also means the trade is increasingly vulnerable to positioning shocks, earnings misses, capex timing concerns, or any sign that the return on incremental AI spend is deteriorating.

The key change is that AI is no longer just a fundamental story; it is a market-structure story. Leverage is building, and volatility across large-cap Tech is expanding relative to the broader market even as prices move higher. This is the hallmark of a crowded secular winner: the theme remains right, but the path becomes more violent. Higher prices attract more capital, more leverage, more options activity, and more systematic participation, which increases the amplitude of both rallies and drawdowns.

Global hedge fund net leverage has climbed to four-year highs, with one of the sharpest four-week increases of the past five years. That increase has been driven by both net buying and mark-to-market gains. This matters because the market’s risk budget is now more exposed to any reversal in the same winners that generated the gains. When leverage rises because positions are working, the system becomes reflexive: performance increases exposure, exposure increases sensitivity, and any reversal can force de-risking.

The broadening story is real, but it is not happening at the expense of AI. Flows have expanded into Financials, cyclicals, Europe, and Asia, but investors are not funding that by abandoning the AI complex. Instead, the composition of AI ownership is changing. Overall US Tech exposure has risen toward five-year highs, while Mag 7 gross and net exposure has fallen to one-year lows. Investors are rotating deeper into the AI ecosystem, especially Semis and Asian chipmakers, rather than simply adding more Mega-Cap exposure.

That rotation deeper into AI makes sense fundamentally. The market is trying to own the beneficiaries of capex and physical deployment rather than only the platform companies funding it. Semis, memory, Asian chipmakers, hardware, power, cooling, networking, and infrastructure names offer more direct leverage to the next dollar of AI spend. But this also means the AI trade is becoming more factor-intensive and less concentrated in stable mega-cap balance sheets. In some ways, the trade may be broader, but also more volatile.

June’s other major takeaway is that macro is back. The Iran deal removed one inflation risk by taking much of the geopolitical premium out of Brent, but the Fed replaced it with renewed policy uncertainty. Warsh’s first FOMC pushed front-end rates higher and reminded investors that falling oil does not automatically mean easier policy. The market now has to recalibrate event-volatility premium more carefully, especially around NFP and FOMC days, where the reaction function is less predictable than it was under the prior regime.

The speed with which investors faded geopolitical risk has been striking. Brent has retraced most of its war premium, managed money has sold nearly $25bn of crude over the past seven weeks, outright shorts have reached new highs after a record build, and net length is now below pre-war levels. That is an aggressive repositioning. Investors have effectively closed the book on oil and shifted attention back to rates, the Fed, and AI. The risk is that this leaves the market exposed if implementation of the Iran deal disappoints or if supply normalization is slower than expected.

Oil’s decline has been a major equity stabilizer. It offsets some of the hawkish Fed impulse by reducing headline inflation pressure, supporting consumers, and easing margin concerns. But if crude positioning is now heavily short, the asymmetry has changed. Lower oil has already been capitalized into risk assets, while any reversal could quickly reintroduce inflation anxiety. The back end of the crude curve remains the cleaner signal of whether investors believe this is a durable regime shift or just an aggressive unwind of war premium.

Systematic flows remain an important amplifier, particularly through leveraged ETFs. Dealer gamma associated with leveraged ETFs can reinforce both upside and downside momentum, and Korea is a prime example given the intensity of AI and chipmaker participation. The stat that leveraged ETF dealer gamma rebalancing can exceed 20% of Korea’s market ADV on large-move days is extremely important. It means that in certain markets, the derivative and leveraged-product ecosystem can become a major flow driver in its own right.

This helps explain why Asia AI has felt so explosive. The fundamental story is strong, but the mechanical flows can intensify the move. When chipmakers rally, leveraged ETF exposure and dealer hedging can add more buying pressure; when they fall, the same process can amplify selling. That makes Korea and Japan critical tells for global AI risk appetite, but also raises the risk of intraday air pockets and feedback loops.

The market’s current state is therefore constructive but fragile. AI remains the highest-conviction secular story, and capital continues to flow toward it globally. Capex revisions, earnings momentum, and adoption are all still supportive. But the market is carrying more length, more leverage, and more structural volatility. That means the correct question is not whether to own AI, but how to own it with better risk control.

The cleaner implementations are likely to be more selective. Investors may prefer diversified AI infrastructure exposure over crowded single-name momentum, Asia chipmakers with earnings revision support over purely conceptual AI beneficiaries, and options structures that define downside in names where leverage and implied volatility are elevated. The old expression of “just own Mag 7” is being replaced by a more complex basket of Semis, memory, networking, power, cooling, industrial infrastructure, Asian hardware, and select software or platform names with proven monetization.

At the same time, macro hedging matters more than it did earlier in the year. A hawkish Fed, stronger dollar, higher front-end rates, or renewed oil spike can all pressure the long-duration and high-beta parts of the AI trade. Event vol should not be priced as casually as it was during the lower-volatility part of the rally. NFP, CPI, and FOMC are now genuine risk-transfer events again, especially with Warsh’s reaction function still being discovered.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!